The log sinh arcsinh distribution is another flexible loss severity candidate family. It is often preferred to summarize the risk with a single default probability and loss severity to simply focus on the expected loss.

Chapter 3 Modeling Loss Severity Loss Data Analytics

Description of frequency severity modeling a more sophisticated frequencyseverity model design ofrequency over dispersed poisson ocapped severity gamma opropensity of excess claim binomial.

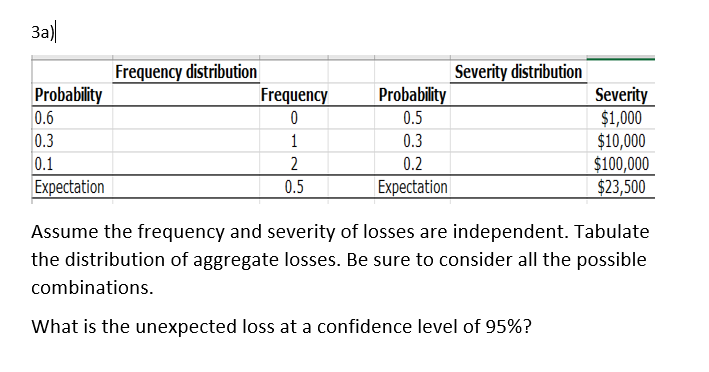

Which probability distribution is used to model loss severity. Truncation probability estimates can be used to identify tail behavior of loss severities. With these two distributions the bank then computes the probability distribution of the aggregate operational loss. Estimation of loss severity distributions vytaras brazauskas and sahadeb upretee.

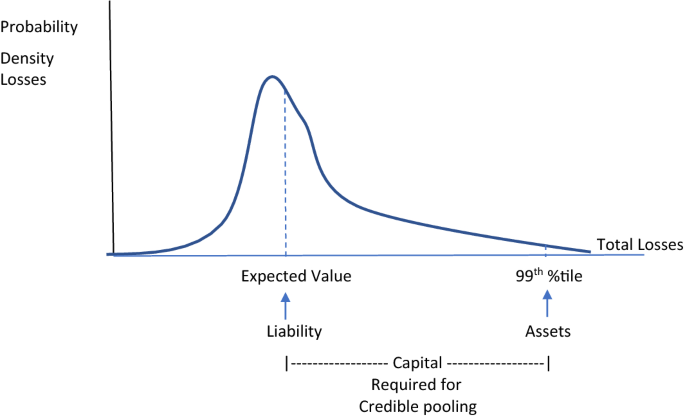

The total required capital is the. 1 note that some authors use model risk. Some examples of such events are loss amounts paid by an insurance company and demand of a product as depicted by its sales.

The quantile score accurately selects severity distributions based on forecast accuracy for a quantile or quantile region. The severity procedure estimates parameters of any arbitrary continuous probability distribution that is used to model the magnitude severity of a continuous valued event of interest. Claim severity has a gamma distribution loss cost claim frequency x claim severity can be much more complex.

Quantiles of probability distributions play a central role in the definition of risk measures eg value at risk conditional tail expectation which in turn are used to capture the riskiness of the. Some examples of such events are loss amounts paid by an insurance company and demand of a product as depicted by its sales. Some examples of such events are loss amounts paid by an insurance company and demand of a product as depicted by its sales.

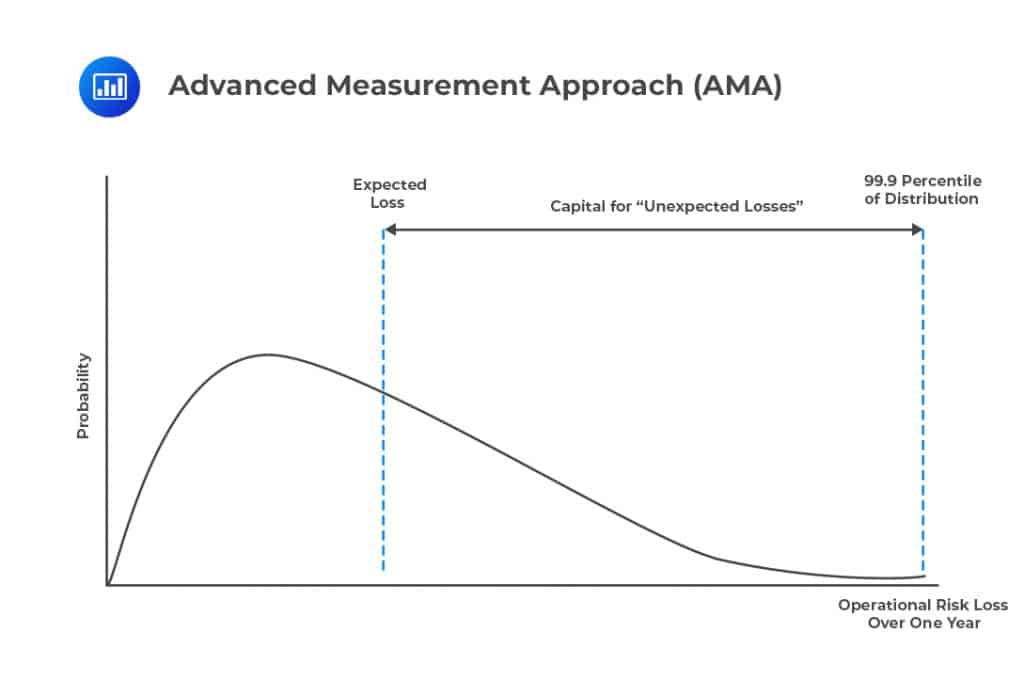

The credit risk is reflected in the distribution of potential losses that may arise if the investor is not paid in full and on time. The traditional loss distribution approach to modeling aggregate losses starts by separately fitting a frequency distribution to the number of losses and a severity distribution to the size of losses. Bank estimates for each business linerisk type cell the probability distributions of the severity single event impact and of the one year event frequency using its internal data.

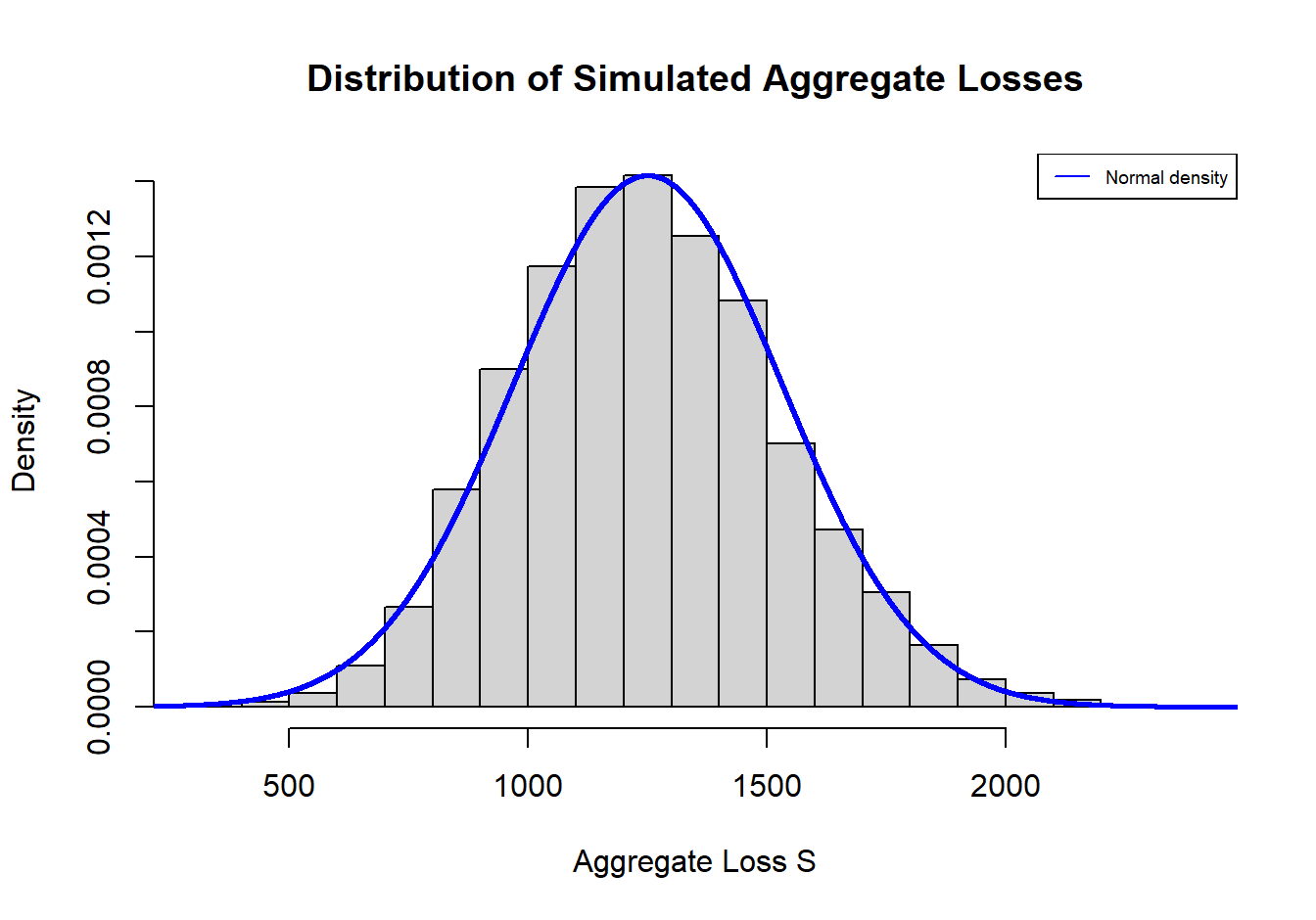

The estimated aggregate loss distribution combines the loss frequency distribution and the loss severity distribution by convolution. Proc severity is especially useful when. The severity procedure estimates parameters of any arbitrary continuous probability distribution that is used to model the magnitude severity of a continuous valued event of interest.

Proc severity is especially useful when. Textexpected loss default probability textloss given default. The severity procedure estimates parameters of any arbitrary continuous probability distribution that is used to model the magnitude severity of a continuous valued event of interest.

Severity Distribution Simple Definition Statistics How To

1 Probability Density Function Of A Model Where High Severity Losses Download Scientific Diagram

Chapter 3 Modeling Loss Severity Loss Data Analytics

Chapter 3 Modeling Loss Severity Loss Data Analytics

Loss Distribution Approach Lda For Ama Of Operational Risk Under The Download Scientific Diagram

Loss Data Analytics

Https Media Neliti Com Media Publications 178763 En None Pdf

Https Media Neliti Com Media Publications 178763 En None Pdf

Chapter 5 Aggregate Loss Models Loss Data Analytics

Https Media Neliti Com Media Publications 178763 En None Pdf

Pareto Distribution Wikipedia

Fdic Supervisory Insights Economic Capital And The Assessment Of Capital Adequacy

Loss Data Analytics R Codes

Loss Data Analytics

Operational Risk Analystprep Frm Part 1 Study Notes

Pdf Approximation Of Aggregate Losses Using Simulation

Loss Data Analytics

Generalized Linear Models For Dependent Frequency And Severity Of Insurance Claims Sciencedirect

Estimating The Distribution Of A Stochastic Sum Of Iid Random Variables In Mathematica Slovaca Volume 70 Issue 3 2020

Severity Modeling Of Extreme Insurance Claims For Tariffication Sciencedirect

Fitting The Gpd To Tail Of Severity Distribution Above Threshold 10 Download Scientific Diagram

Pdf Approximation Of Aggregate Losses Using Simulation

Risks Free Full Text Multivariate Frequency Severity Regression Models In Insurance Html

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gctila1xx2ltdhyqjbjtpcyxa8qfxzhm4krefhfh N Thlok5943 Usqp Cau

Insurance For Economic Losses Caused By Pandemics Springerlink

Pdf Mixed Distributions For Loss Severity Modelling With Zeros In The Operational Risk Losses

Insurance Risk Pricing Tweedie Approach By Ajay Tiwari Towards Data Science

Za Frequency Distribution Probability Frequency 0 Chegg Com

Estimating The Distribution Of A Stochastic Sum Of Iid Random Variables In Mathematica Slovaca Volume 70 Issue 3 2020

Insurance For Economic Losses Caused By Pandemics Springerlink

Https Www Casact Org Pubs Forum 05spforum 05spf215 Pdf

Pdf Mixed Distributions For Loss Severity Modelling With Zeros In The Operational Risk Losses

Https Www Casact Org Pubs Forum 05spforum 05spf215 Pdf

Taken To Excess The Actuary

Severity Modeling Of Extreme Insurance Claims For Tariffication Sciencedirect

Modeling Insurance Claim Severity By Ajay Tiwari The Startup Medium

Modeling The Frequency And Severity Of Auto Insurance Claims Using Statistical Distributions

Modeling Operational Risk Alexander Johnemark Pdf Free Download

Modeling Insurance Claim Severity By Ajay Tiwari The Startup Medium

Https Media Neliti Com Media Publications 178763 En None Pdf

Https Www Casact Org Library Astin Vol27no1 117 Pdf

An Analysis On Operational Risk In International Banking A Bayesian Approach 2007 2011

Loss Data Analytics

Pdf Credit Risk Measurement Of Securitization Tranches

Modeling The Frequency And Severity Of Auto Insurance Claims Using Statistical Distributions

Https Arxiv Org Pdf 1008 1108

An Analysis On Operational Risk In International Banking A Bayesian Approach 2007 2011

Severity Modeling Of Extreme Insurance Claims For Tariffication Sciencedirect

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcqezyygaidkggbjun62qkdlghfrdscoegae0zxpfb4hdtvdvr6t Usqp Cau

Http Www Iam Fmph Uniba Sk Institute Jurca Qrm Chapter5 Pdf

Https Virtusinterpress Org Img Pdf 10 22495 Jgr V2 I3 P5 Pdf

Https Cran R Project Org Web Packages Opvar Vignettes Opvar Vignette Html

Risks Free Full Text Multivariate Frequency Severity Regression Models In Insurance Html

Chapter 3 Risk Measurement Ppt Download

Https Sites Uwm Edu Vytaras Files 2016 04 2016 Naaj Final Pvdlsn Pdf

Risk Management Wikipedia

Https Virtusinterpress Org Img Pdf 10 22495 Jgr V2 I3 P5 Pdf

Pdf The Determinants Of Frequency And Severity Of Operational Losses In Tunisian Insurance Industry

Quantifying The Risk Of Natural Catastrophes Understanding Uncertainty

Operational Risk Analystprep Frm Part 1 Study Notes

Loss Data Analytics

Probability Distribution An Overview Sciencedirect Topics

Pareto Distribution Wikipedia

An Analysis On Operational Risk In International Banking A Bayesian Approach 2007 2011

Https Www Mdpi Com 2227 9091 4 1 4 Pdf

Https Www Scor Com En File 33967 Download Token I 5u8wl

Modeling Operational Risk Alexander Johnemark Pdf Free Download

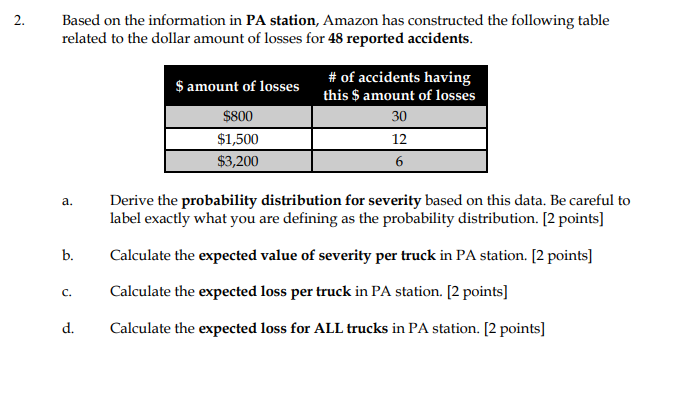

Solved 1 The Amazon Com Inc Owns Trucks Used For Cargo Chegg Com

Https Citeseerx Ist Psu Edu Viewdoc Download Doi 10 1 1 176 1327 Rep Rep1 Type Pdf

Pdf Approximation Of Aggregate Losses Using Simulation

Https Www Casact Org Pubs Forum 05spforum 05spf215 Pdf

Estimating The Distribution Of A Stochastic Sum Of Iid Random Variables In Mathematica Slovaca Volume 70 Issue 3 2020

Modeling Insurance Claim Severity By Ajay Tiwari The Startup Medium

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcrrop7lovqrkxwke5ymag0paowx7h5xuplupm16ykphqdngw0mx Usqp Cau

Evolving Risk Management Fundamental Tools

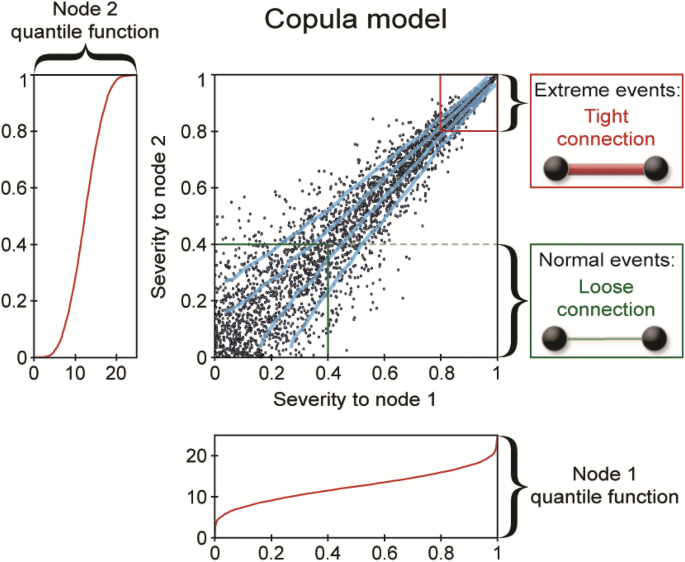

Integrating Systemic Risk And Risk Analysis Using Copulas Springerlink

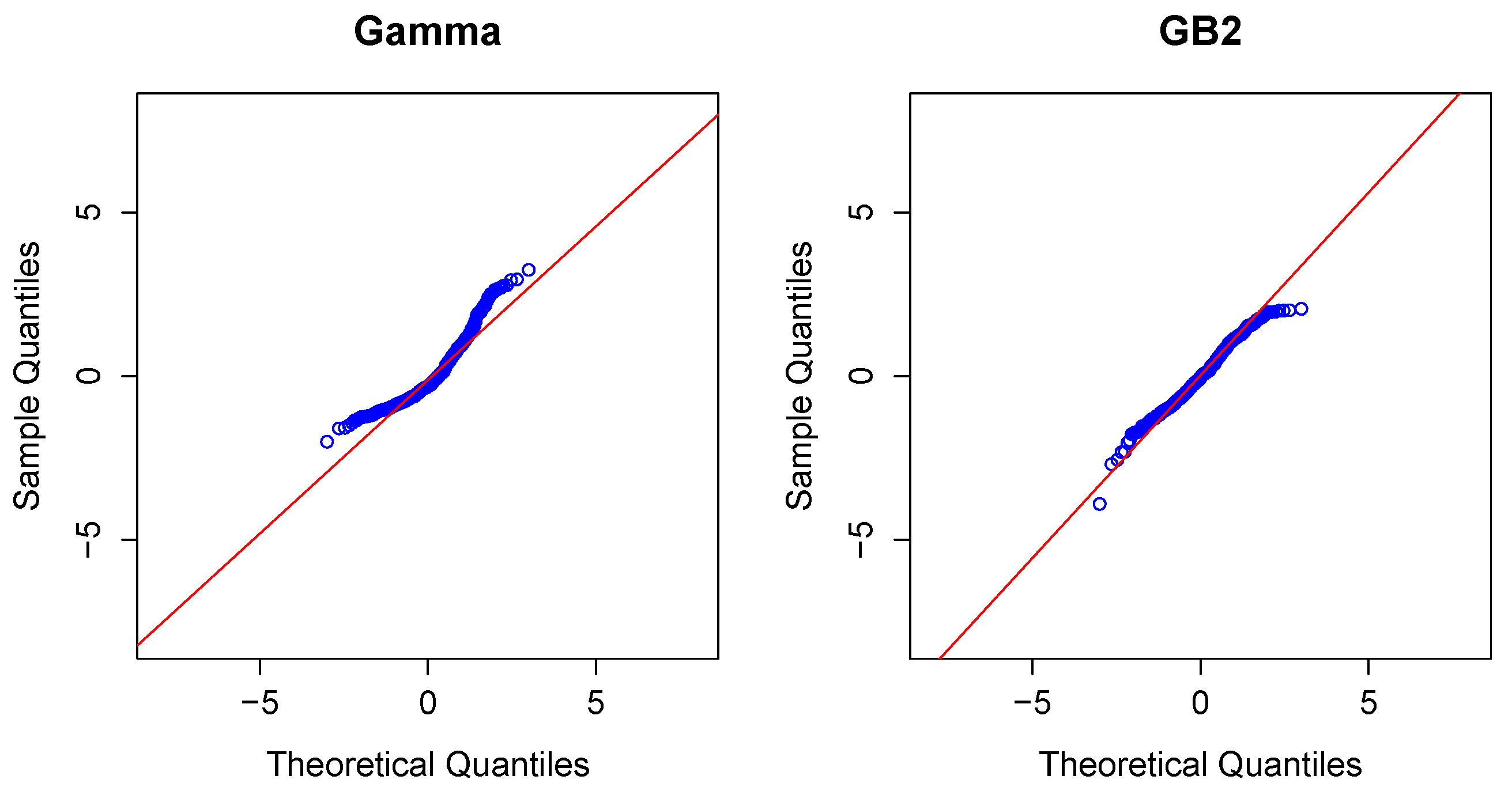

On The Selection Of Loss Severity Distributions To Model Operational Risk Journal Of Operational Risk

Https Arxiv Org Pdf 1808 06718

Https Www Casact Org Library Studynotes Grossi Kunreuther Errata07 02 13 Pdf

Https Virtusinterpress Org Img Pdf 10 22495 Jgr V2 I3 P5 Pdf

Ijfs Free Full Text Operational Risk Management In Financial Institutions A Literature Review Html

Probability Distribution An Overview Sciencedirect Topics

Https Faculty Unlv Edu Pthistle Fin321class Lecturenotes Chapter3 Pdf

Modeling Insurance Claim Severity By Ajay Tiwari The Startup Medium

Pdf Approaches To Modeling Operational Risks Of Frequency And Severity In Insurance

Https Www Jstor Org Stable 252434

Loss Data Analytics R Codes

Https Www Jstor Org Stable 251860

Contributions Of Frequency Distribution Analysis To The Understanding Of Coronary Restenosis Circulation

A Maximum Entropy Approach To The Loss Data Aggregation Problem

Https Virtusinterpress Org Img Pdf 10 22495 Jgr V2 I3 P5 Pdf

Http Ies Fsv Cuni Cz Default File Download Id 8910

A Limit Distribution Of Credit Portfolio Losses With Low Default Probabilities Sciencedirect

An Analysis On Operational Risk In International Banking A Bayesian Approach 2007 2011

Https Faculty Unlv Edu Pthistle Fin321class Lecturenotes Chapter3 Pdf

Https Www Casact Org Pubs Forum 05spforum 05spf215 Pdf

Https Pdfs Semanticscholar Org C77e F9111c98fc81c7636f18740f51b877608804 Pdf

Https Core Ac Uk Download Pdf 211518053 Pdf

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcq3bkktfwdbcunhyygddvzlano Dlkgcahdyaicftyxe Iunhtq Usqp Cau

Modeling Insurance Claim Severity By Ajay Tiwari The Startup Medium

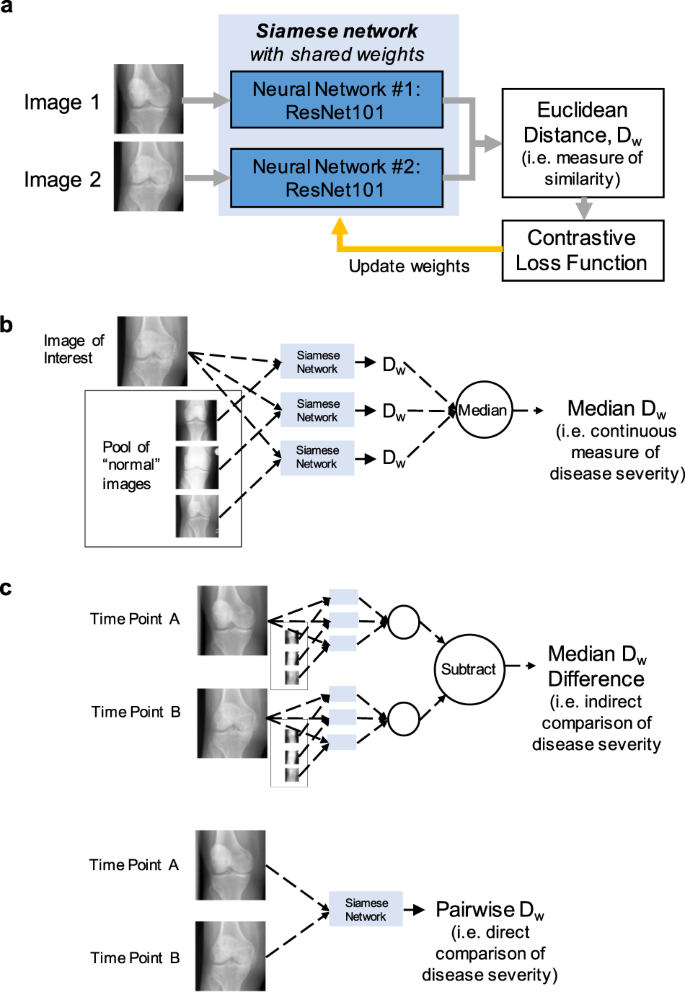

Siamese Neural Networks For Continuous Disease Severity Evaluation And Change Detection In Medical Imaging Npj Digital Medicine

Managing Operational Risk Ama Ppt Download

Modeling Loss Data Using Mixtures Of Distributions Sciencedirect

Post a Comment for "Which Probability Distribution Is Used To Model Loss Severity"